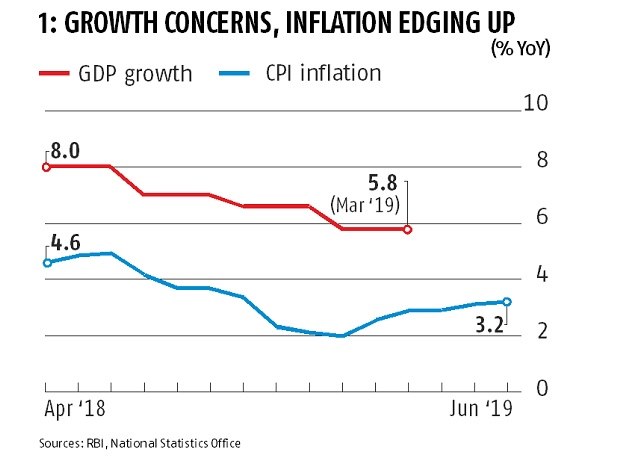

The Reserve Bank of India’s monetary policy committee (MPC) will meet this week, and is likely to reduce policy rate further to help revive the economy. Benign inflation and falling economic growth, as shown in Chart 1, are the basic indicators that make the case to continued easing of monetary policy.

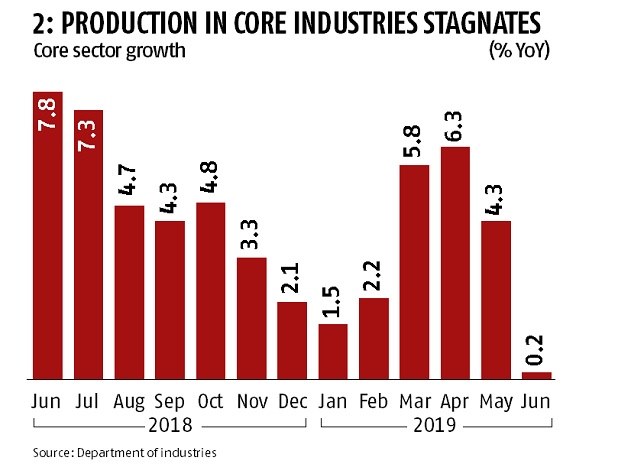

High frequency data point in the same direction. Production in core industries such as steel, cement, oil and coal grew at a paltry 0.2 per cent in June, lowest in more than four years (Chart 2). There is no growth in sight in auto sector either (Chart 3). A rate cut with monsoon getting better by the day (Chart 4) could help improve consumption.

Further, following the Union Budget’s announcement of income tax surcharge on foreign portfolio investors (organised as trusts) sent foreign capital packing in July, after pouring in for five months (Chart 4). Loosening of credit channels can potentially improve business sentiment and reverse this capital outflow.

Also read: Economic Survey 2019 Envisions India Rebounding on the Back of Private Investments

In addition to the fact that monetary policy is inherently limited in its efficacy to boost growth, monetary transmission has been poor in this cycle. Lending rates did not move down much after the first two rate cuts of 2019 (Chart 5).

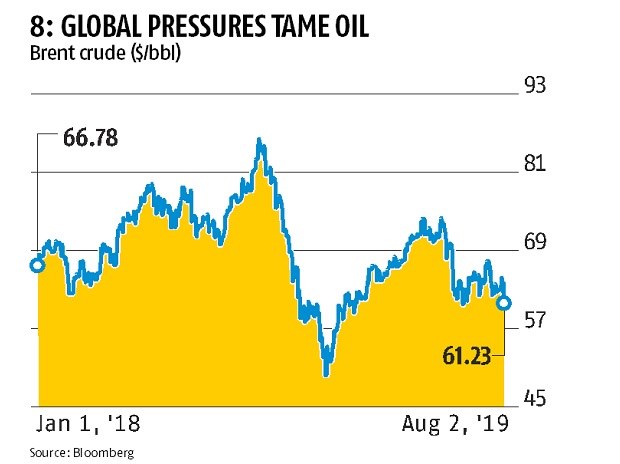

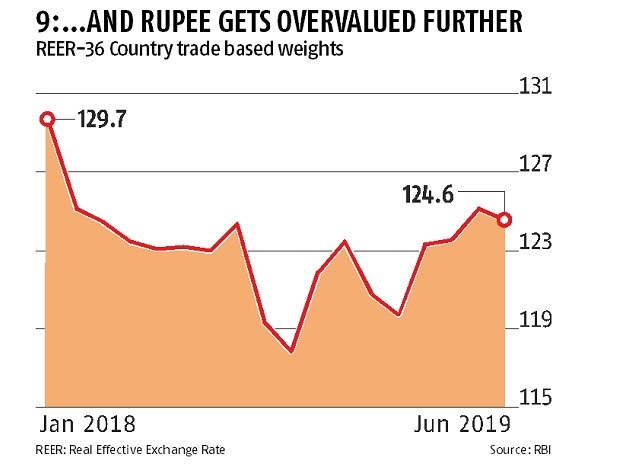

On the external front, the rupee has largely strengthened since October 2018 (Chart 6), one of the principal reasons being favourable to oil prices (Chart 7). But the strength of the rupee has made it more overvalued than before (Chart 8), affecting exports, which are a crucial catalyst for economic revival.

By arrangement with Business Standard.